The United Kingdom’s Emissions Trading Scheme (UK ETS)

01/10/2020

2020 is shaping up to be a milestone year for aviation in more aspects than anticipated. The global crisis has forced operators to rapidly shift priorities to manage their financial situations in one of the most volatile periods in history. From bankruptcies to total restructuring, from travel restrictions to complete suspension of operations, from CORSIA baseline change to the introduction of Swiss and UK ETS, 2020 has given the industry a lot to grapple with. It is inspiring to see that despite all the hurdles and potential excuses that the year has offered, most nations around the world are unwaveringly committed to positive climate actions.

Period 2020

The United Kingdom in July 2020 committed to the creation of an independent UK ETS, which may in the future be linked to the EU ETS. However, this does not impact the applicability of EU ETS on the 2020 monitoring period. During the transition period, from 1st February to 31st December 2020, the UK will remain a full participant in the EU ETS which implies that participating UK operators must meet their 2020 compliance obligations. Furthermore, considering the recent EU-Swiss ETS linking agreement, the scope of emissions that must be reported for 2020 has increased. Operators should ensure all emissions on flights between the UK, EEA and Switzerland are included in their 2020 emissions report, and that allowances to cover this increased scope are surrendered by 30 April 2021.

A summary of the UK ETS

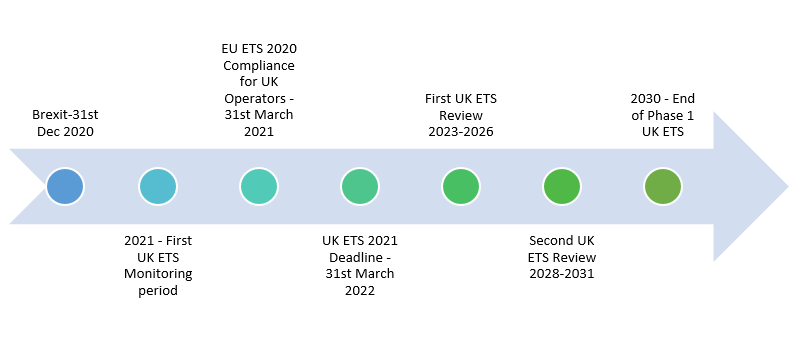

UK ETS will start on 1st January 2021 with the year 2021 the first monitoring period, and 31st March 2022 the first reporting deadline. In essence, the UK ETS is to a great extent similar to the EU ETS with most design features mirroring its predecessor. It is unclear whether the UK government will be able to finalize a linking agreement with the EU Commission before the 2021 reporting obligations.

From a timeframe perspective, the first phase of UK ETS is slated to last from 2021-2030 with two full system reviews. The reviews will aim to discuss, introspect and implement changes to the rules and overall design of the UK ETS as may become necessary with future developments.

The UK government has chosen to not allow offsets in the UK ETS, which implies that the UK ETS would not be compatible with CORSIA. They have instead affirmed that they will review their position on CORSIA and offsets during the first review. The surrendering obligations will most probably be delayed considering that negotiations with the EU and ICAO are underway.

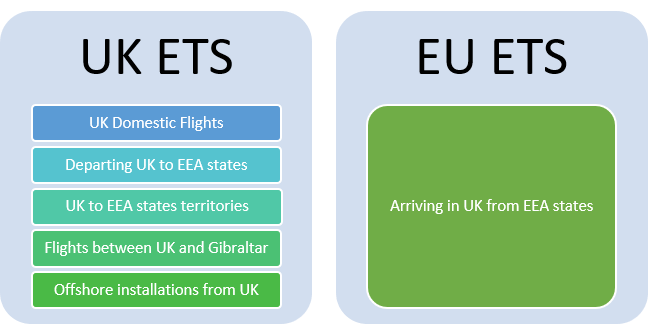

The UK ETS will encompass all UK domestic flights as well as flights departing from the UK to EEA states and its territories. It will also impose surrendering obligations on flights between Gibraltar, offshore installations and the UK. All flights arriving in the UK from EEA, will on the other hand continue to be covered by the EU ETS in case a link agreement is reached.

The UK government plans to implement an aviation emissions cap which would be equivalent to the UK’s estimated share within the EU ETS phase IV aviation cap. Accordingly, the free allocation of allowances will be done for each operator based on their historic activities on the routes which are covered by the UK ETS. Subsequently, the allocated allowances will reduce annually by 5%, in line with the reducing aviation cap.

Thresholds and exemptions

In all scenarios (linking or no linking), the thresholds for commercial and non-commercial aircraft operators would be the same as those in the current EU ETS.

Under UK ETS, full scope activity is defined as all flights that either arrive or depart from an aerodrome within the UK, Gibraltar or European Economic Area (EEA), regardless of where the aircraft operator is registered.

Similarly, the reduced scope would refer solely to domestic UK flights and flights departing from the UK to EEA states and its territories.

All thresholds will be based upon the full scope activity while all surrendering obligations would be calculated based on the UK ETS reduced scope.

Flights operated by fixed wing and rotary wing aircraft would be included unless the MTOW (maximum takeoff mass) is below 5700 Kg. Helicopters are subject to MRV under UK ETS just like they were under EU ETS.

Commercial aircraft operators would not be subject to any obligations if they meet either of the following criteria:

• Operate fewer than 243 flights per period for three consecutive four-month periods based on full scope activity. The four-month periods are: January to April, May to August, September to December,

• Operate flights with total annual emissions less than 10,000 tonnes of CO2 per year based on full scope activity.

Non-commercial aircraft operators would not be subject to any obligations if they operate flights with total annual emissions lower than 1,000 tonnes of CO2 per year based on full scope activity.

The UK ETS will require a new emissions monitoring plan and will initially only allow for the use of the same two methods that are permitted in the EU ETS. The UK Government aims to make the UK ETS compatible with CORSIA, to allow all five methods but it is not clear when this would be achieved.

The UK ETS is building on the rich legacy of the EU ETS to achieve the 2050 net zero goal. It is a good example for other countries to follow and set up their own emissions trading schemes to account for all types of emissions that they produce, or to consider extending CORSIA to include domestic flights.

> Click here for more detailed information on UK ETS

> UK ETS FAQ's are available here

> UK ETS Summary in French (Source: DGAC)

> UK government sets out plans for including aviation in its own emissions trading scheme from next year (GreenAir Online)